The Mutual Fund 7-5-3-1 Rule: A Proven SIP Strategy for Wealth

Two questions come up almost every time someone starts their investing journey: How long should I stay invested? and How do I plan my SIPs?

For new Indian investors often asking, "mutual fund kya hai?" (what is a mutual fund?), understanding the core mutual fund meaning is just the first step. The real secret to building wealth isn't just picking the right fund—it's having a system. The mutual fund 7531 rule is exactly that framework. It relies on four specific numbers, each doing a dedicated job to protect your portfolio from market noise and human emotion.

Before You Start: The Liquidity Check

Don't lock money into a 7-year equity strategy if you might need it next month. Get 6 months of living expenses into a liquid fund or savings account first. Without that buffer, you'll end up selling equity funds at the worst possible time — during a market dip, to cover an emergency.

Want to go deeper on Mutual Funds?

We've written a dedicated guide covering fund types, NAV, expense ratios, how to pick the right fund, and how to actually start investing — step by step.

Read: Mutual Funds Explained — From Basics to Investing →What is the Mutual Fund 7531 Rule?

Four numbers. Used together, they push back against the most common SIP mistakes — quitting too early, betting everything on one theme, ignoring how emotions work, and letting contributions go stale against inflation.

7 — Stay Invested for 7 Years

Equity markets are noisy in the short run. Seven years gives compounding enough time to show up in your numbers — and it smooths out most of the volatility that would otherwise push you to exit at exactly the wrong moment.

5 — Diversify into 5 Strategies

Spread your SIPs across different strategies — Large-cap, Mid/Small-cap, Flexi-cap, Value/Contra, and Global funds. When doing a mutual fund comparison, the goal isn't diversity for its own sake. It's avoiding the trap of having everything tied to a single style when that style goes out of favour.

3 — Expect 3 Emotional Phases

You'll feel disappointed when returns are modest, frustrated when they're flat, and panicked when the market drops. Knowing these phases are coming stops you from treating a normal downturn like a signal to bail. The "3" also covers asset classes: equity, debt, and gold.

1 — Increase Your SIP by 10% Every Year

A 10% bump annually doesn't feel like much in year two. By year fifteen, it creates a very different corpus. Flat contributions slowly lose ground to inflation — the step-up is how you keep pace.

Why Bother With an Investing Rule at All?

Much like the popular mutual fund 75 5 10 rule (which focuses heavily on asset allocation: 75% equity, 5% liquid, 10% gold), the 7-5-3-1 rule provides a structural discipline. It helps because:

- It keeps you invested long enough for compounding to matter.

- It stops you from over-concentrating in whatever sector is trending right now.

- It prepares you for market cycles instead of being blindsided by them.

- It ties your SIP contribution growth to your income growth.

Struggling with Market Swings?

If the "3 emotional phases" sound all too familiar, learning how to handle red days in your portfolio is crucial for long-term success.

Read: Navigating Market Volatility →Things to Watch Out For

The 7-5-3-1 rule is a framework, not a magic formula. Fund quality still matters. Whether you invest directly or through a mutual fund distributor, keep an eye on expense ratios and exit loads. Furthermore, while the mutual fund vs etf debate is ongoing, this rule can technically apply to SIPs in broad-market ETFs as well.

Remember: Step-ups only help if they're within your budget — don't force a 10% increase if it's going to stress your cash flow.

The Part Most People Skip: Portfolio Rebalancing

Spreading across 5 strategies is step one. But allocations drift over time. If your Mid-Cap funds have a massive bull run, they might quietly go from 30% of your portfolio to 60%. Suddenly, you're carrying twice the risk you originally intended.

The Fix: Once a year, check your allocation. If anything has drifted more than 5–10% from your original plan, rebalance. You're trimming what's run up and adding to what's lagged. Scheduling this makes the process mechanical, removing the emotion from the equation.

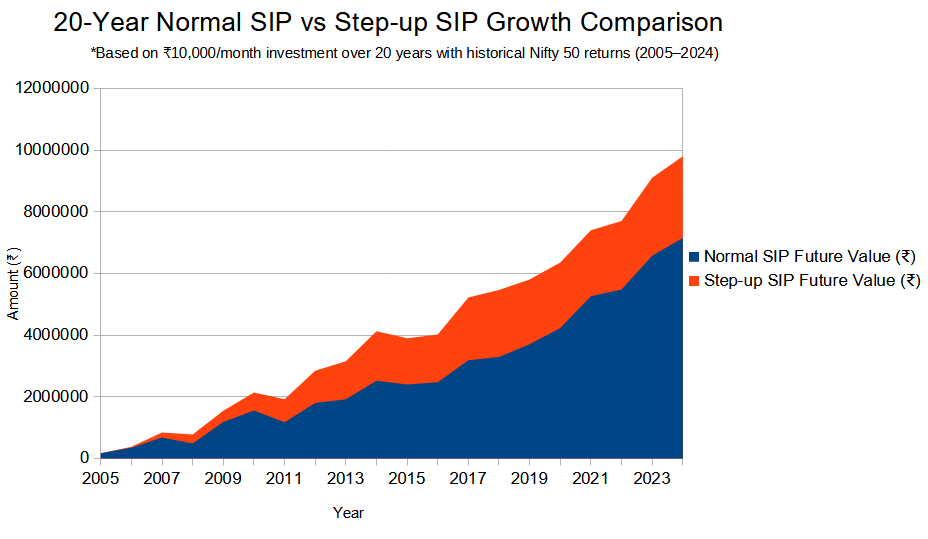

What Step-Up SIPs Actually Look Like

Let's compare a flat ₹10,000/month SIP versus a 10% yearly step-up over 20 years. If you plug these numbers into a standard mutual fund calculator, the step-up corpus ends up roughly double. It's not a trick; it's just compounding working on larger contributions every year.

Analyzing the Data

Both SIPs grow, but the step-up version pulls ahead significantly. Because you're contributing more each year, more money enters the market earlier, granting it more time to compound. Because the chart uses actual Nifty 50 returns, the 2008 crash, 2009's recovery, and 2011's rough patch are all accounted for.

Key Takeaways from the Numbers:

- Both SIPs build real wealth: Even the flat one. This data isn't an argument against flat SIPs — it's an argument for getting started today.

- The gap is small early, massive later: Increasing your SIP in year one matters far more than doing it in year fifteen because the compounding horizon is longer.

- The dips are real: Using actual Nifty 50 data means the corpus drops in bad years. It recovers. That pattern is exactly why the "7-year minimum" rule exists.

Don't Forget the Tax Bill

A mutual fund return calculator showing a ₹5 Crore final value is exciting, but the number you actually get to spend is post-tax. Long-Term Capital Gains (LTCG) on equity mutual funds are taxed at 12.5% on gains above ₹1.25 Lakhs in a financial year. Build the tax into your target number from the start, rather than treating it as a surprise at the end.

Planning for the Long Term?

See how rules like 7-5-3-1 fit into a broader retirement strategy, and learn how to construct a portfolio that you can eventually live off of safely.

Read: Building a Retirement Portfolio with Mutual Funds →Final Thoughts

The 7-5-3-1 rule won't magically outperform the market for you. What it does is give you a repeatable, stress-free structure: stay invested long enough, diversify across strategies, expect your emotions to get tested, and nudge your contributions up every year.

None of it is overly complicated. The hardest part is simply sticking to the plan when the market makes you want to do something dramatic. Ultimately, this rule is your best mechanism for pre-committing to doing nothing dramatic, allowing your wealth to quietly grow in the background.

Knowing the rule is easy. Following it is hard.

The math behind a Step-Up SIP is simple. But having the psychological discipline to continue investing when the market crashes 20%? That is where most people fail. That is where a professional financial advisor steps in. At Earthen Capital, we don't just build portfolios; we manage investor behavior.

Completely